303: Reporting Q&A - February 4, 2025

The Producer Reporting Q&A is a monthly opportunity for producers, their legal representatives, and trade associations to learn about and discuss priority producer issues. Please do not share this content beyond the group.

Presentation

Key Messages

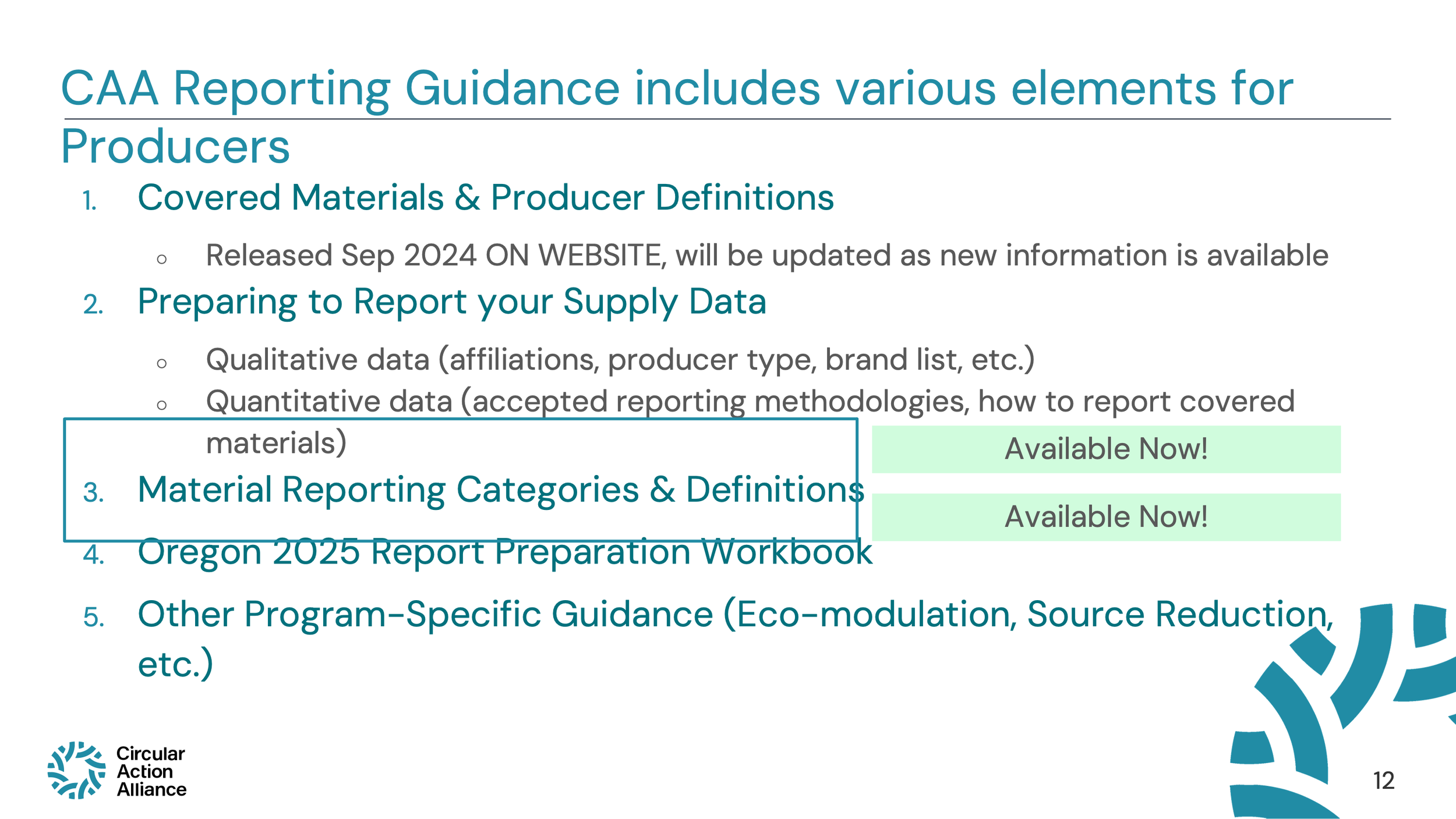

New Guidance now available on our guidance site:

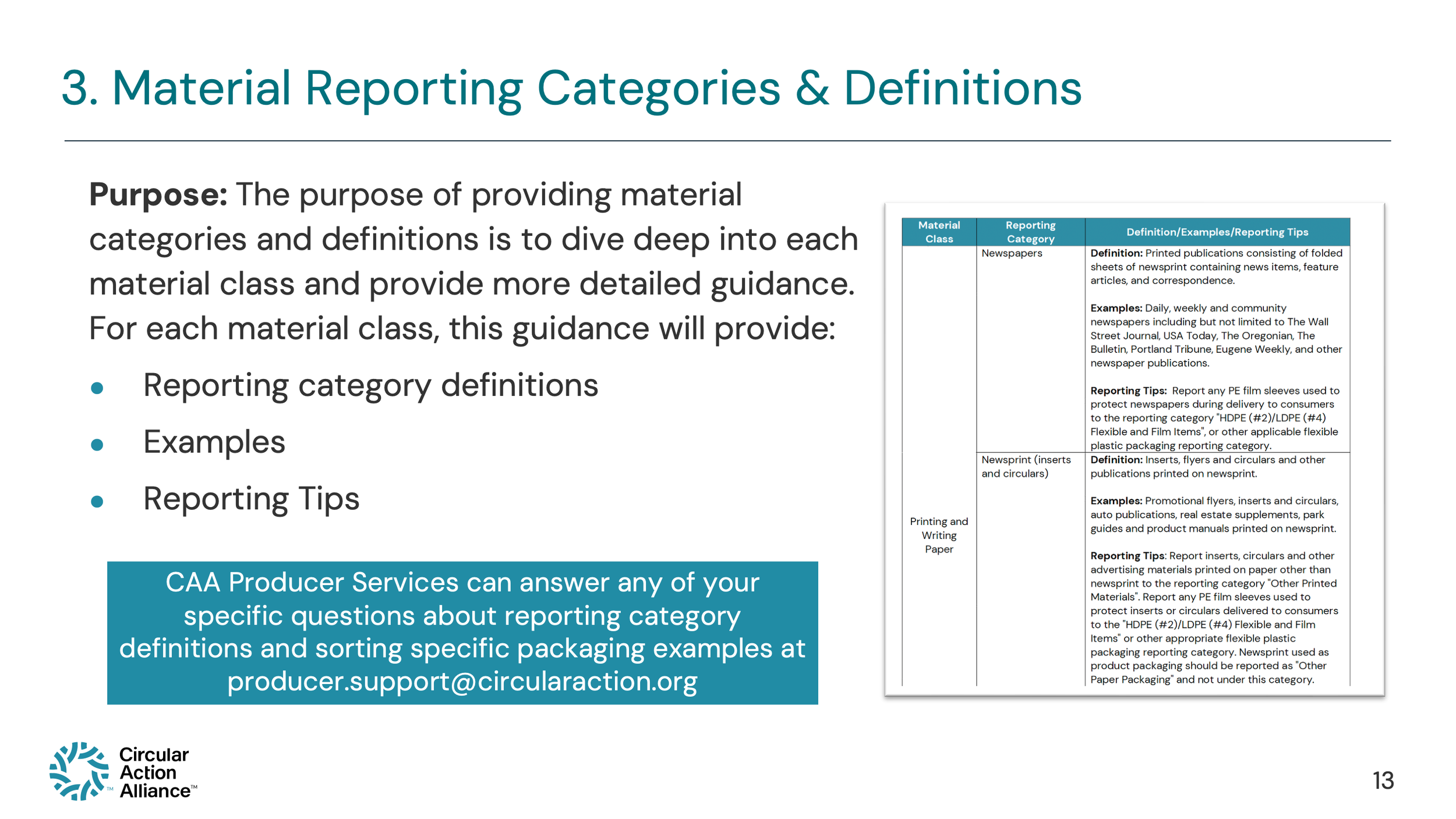

Material Reporting Categories & Definitions: The purpose of this document is to dive deep into each material class and provide more detailed guidance.

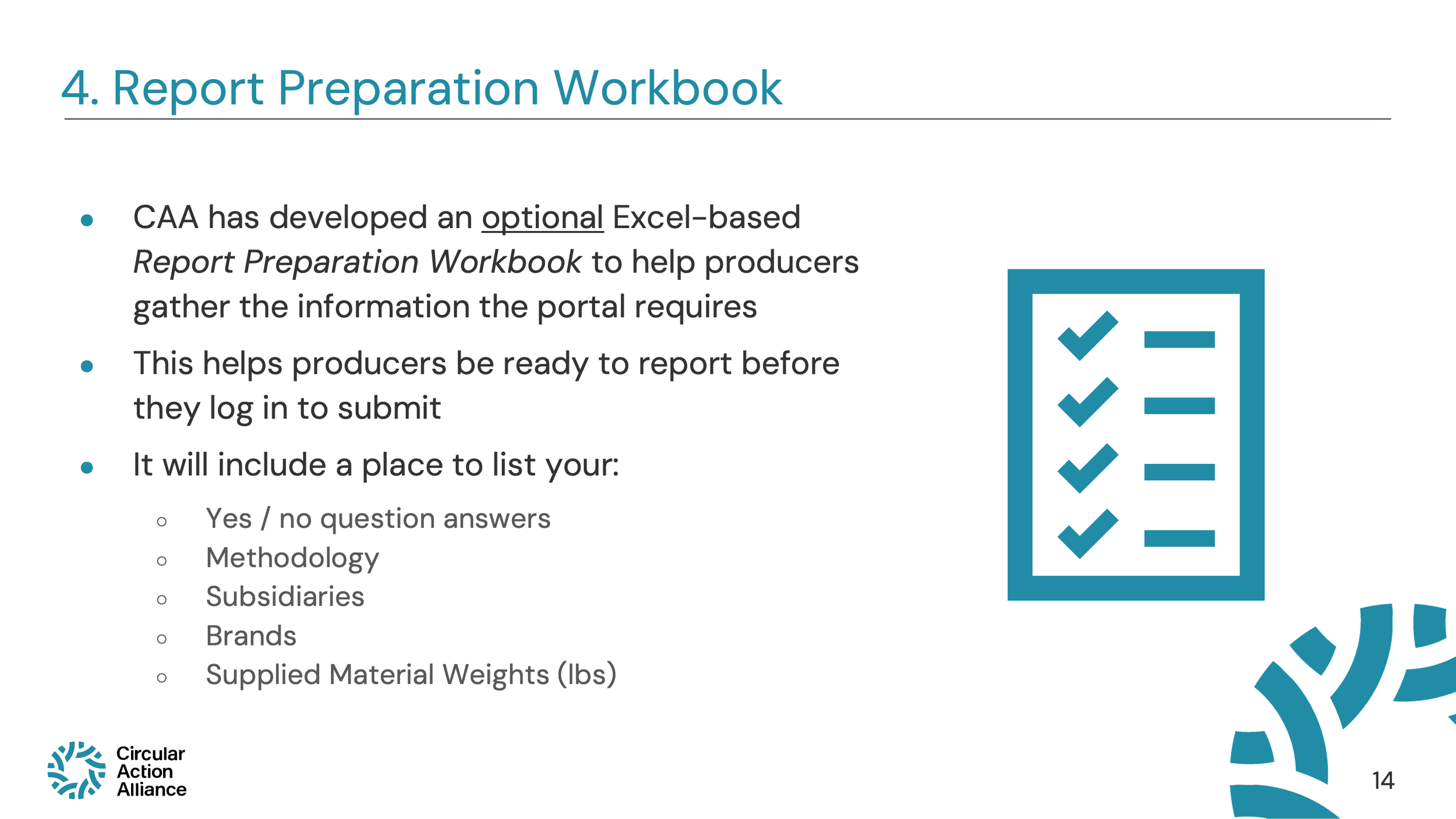

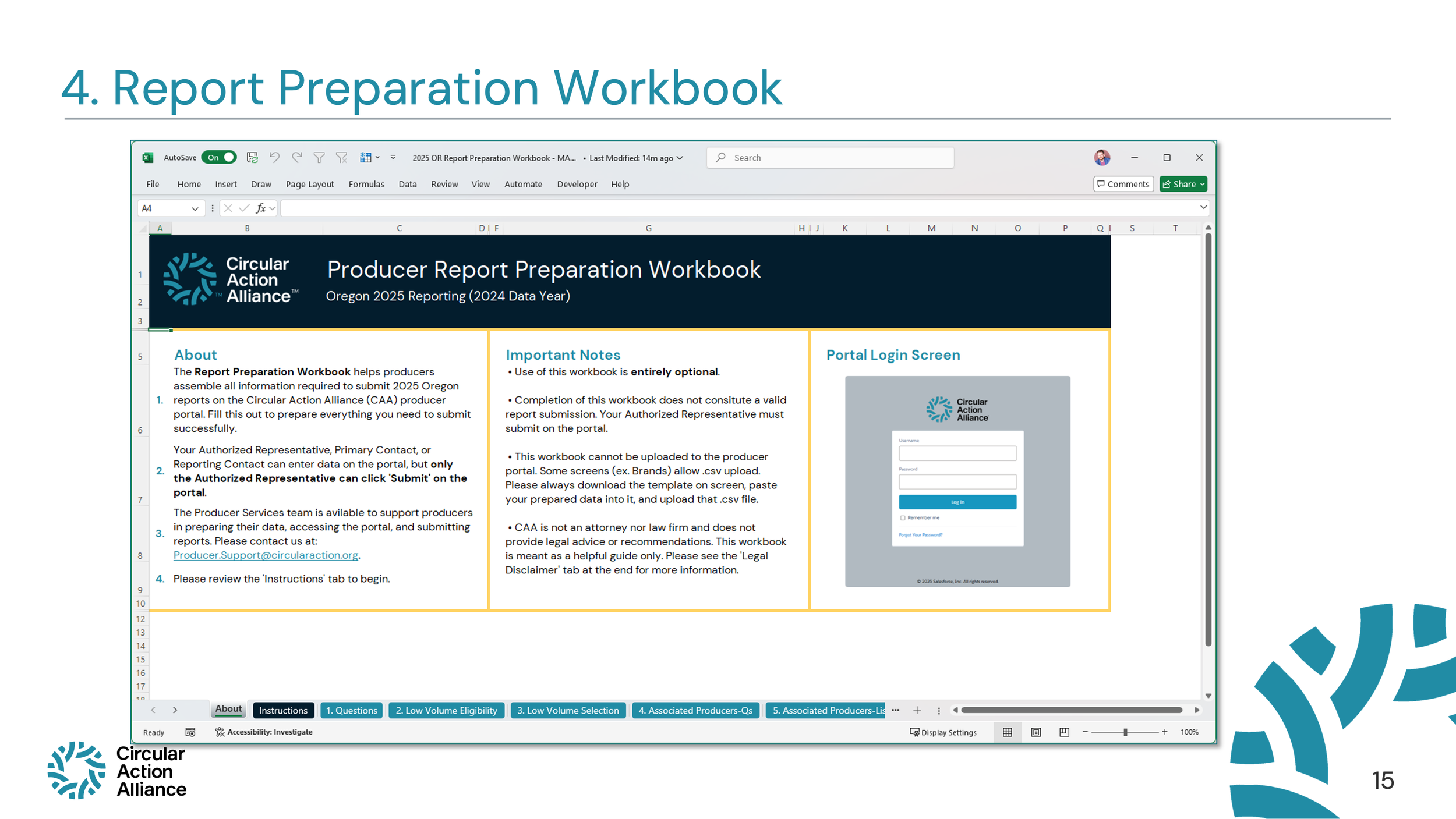

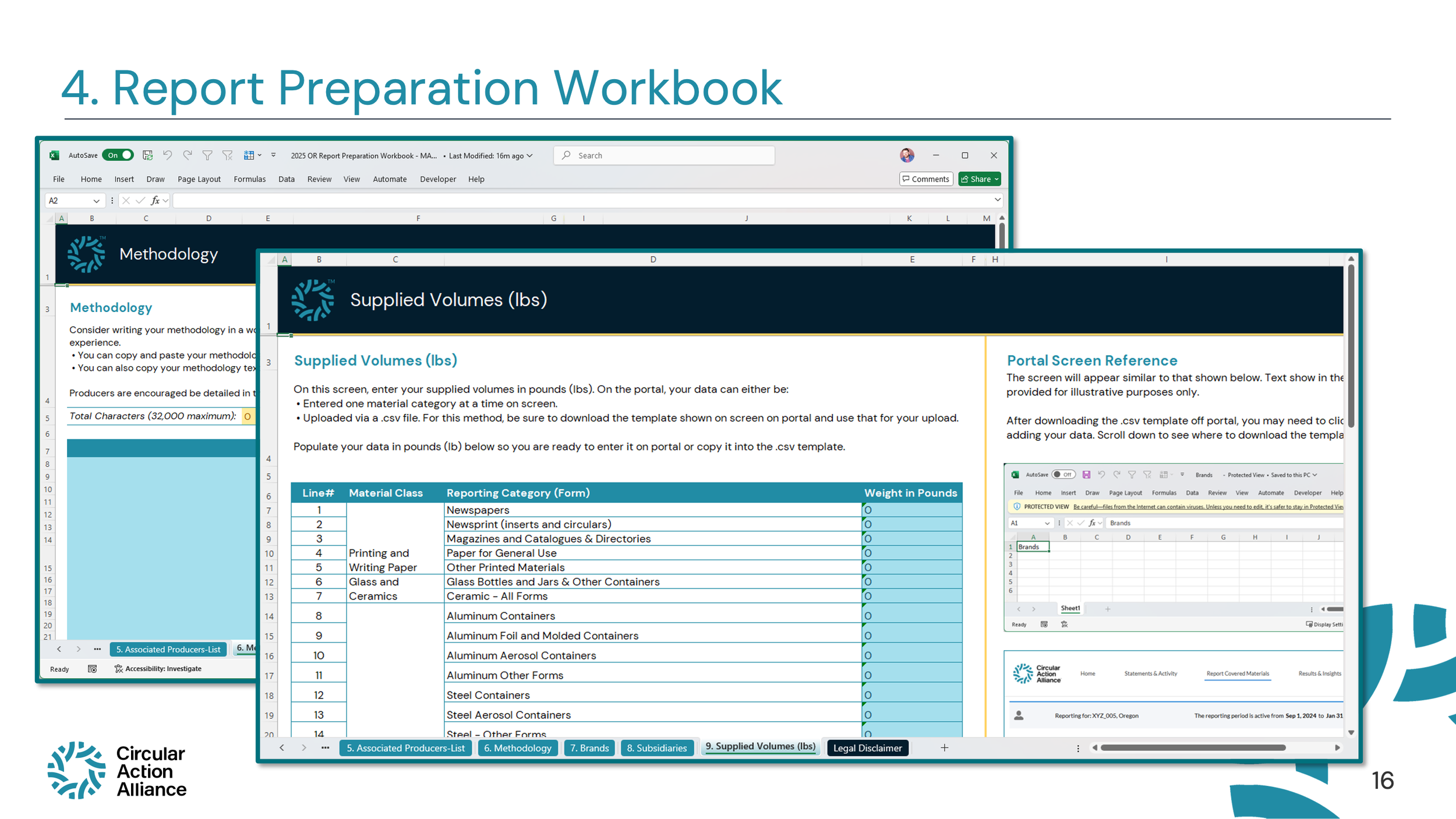

Oregon 2025 Report Preparation Workbook, CAA has developed an optional Excel-based Report Preparation Workbook to help producers gather the information the portal requires

If your question didn’t get answered, please first review the new guidance documents and see if the examples provided help answer your question. If the question is still not answered, please reach out to producer.support@circularaction.org. Please allow about five business days for a response, especially if it is a complicated question as we may be seeking support from others in the organization to find you an answer.

Q&A Overview

-

The preferred method for reporting is to be as specific as possible. If you need to make some level of estimations, you can do so with an average bill of materials. CAA does not provide sector-specific calculators, tools that estimate packaging weights based on industry norms, since using these calculators is generally less accurate. They should be relied upon only in cases of significant data gaps where other reporting methodologies are not feasible. Producers using sector calculators must disclose the methodologies applied, including details of any assumptions or averages used, as part of their reporting submission. Furthermore, the use of sector calculators may not be permitted indefinitely.

You can find out more on page 10-15 of the “Preparing to report your supply data” guidance on our guidance page.

-

If you cannot obtain state-specific sales data for products or services supplied through retailers or vendors, you may use a formula to estimate sales for each applicable EPR state that is outlined in our guidance. This apportionment method should be used only when actual point-of-sale data from retail partners is unavailable, as direct sales data provides a more accurate reflection of supply for the reporting year.

Even when national apportionment is used to estimate units supplied in each state program, Producers are still responsible for ensuring that their reported data accurately reflects their supply in Oregon, and the methodology used and submitted reports are subject to substantiation by CAA.

You can find out more on page 9 and the formula is on page 10 of the “Preparing to report your supply data” guidance on our guidance page.

-

While the portal will accept numbers with many numbers after the decimal points, we recommend including data rounded to no more than 2 decimal places. Reporting done in whole pounds is also fine. If your data requires adding many numbers together that all have varying numbers of decimal points, you will want to be mindful of when your rounding occurs so as not to skew your data. Rounding should be done on the final aggregate numbers where possible.

When reporting to CAA, producers must submit all methodologies used for data preparation. Upon request, producers may be asked to provide additional calculations, substantiation for updates, or estimates to confirm the data's reasonability. This practice promotes fairness and supports accurate fee-setting across all producers. CAA will ultimately perform report validations and may contact producers for clarification or to verify additional data. This step ensures that all reported information meets the required standards and aligns with program guidelines.

-

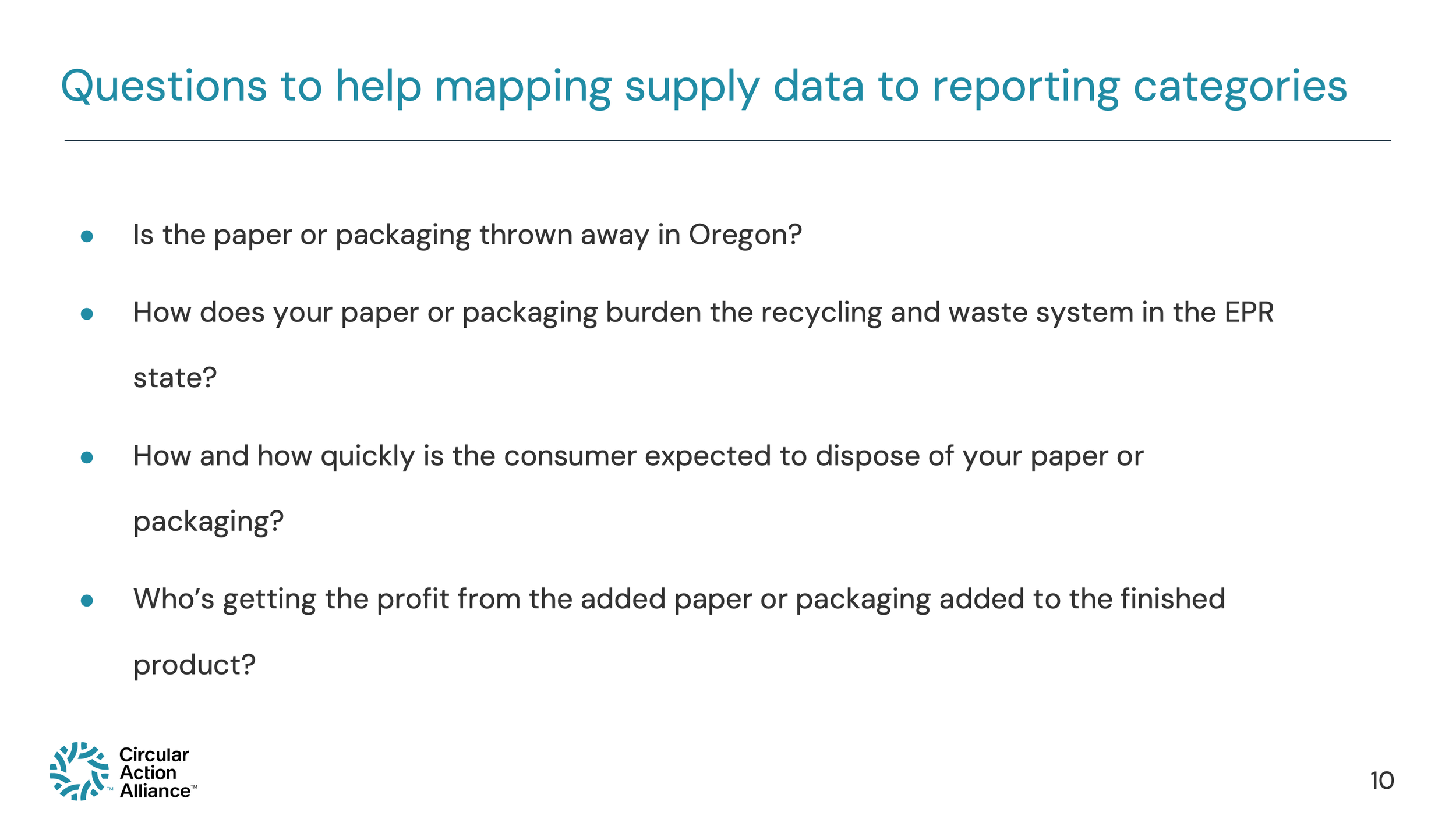

We are asking that companies report a total number of pounds sold into the state. Therefore, if you have unique quantities per SKU or within a SKU, we recommend you follow a specific material reporting method, outlined on page 10 “Preparing to report your supply data” guidance or the best available methodology as found on our guidance page. If you need to distinguish between certain scenarios within a particular SKU you can do that in your reporting and then provide that detail in your methodologies. However, the final number we will ask is a total pounds per reporting material.

-

This depends on if they are separable or non-separable. Separable components are those that can be removed from the main packaging by the end user, either after opening or after the product is consumed. All separable components should be reported separately in the appropriate material category that best fits their material type and form.

Non-separable components are designed to remain attached to the packaging after the product is consumed and discarded. If a component, like a cap or lid, is intended to stay with the package when discarded, or there are on-pack instructions directing the consumer to replace the cap prior to disposal, it is considered a non-separable component for reporting purposes. Non-separable components should be reported in the category representing the material type that makes up the majority of their combined weight

You can find out more on page 16 of the “Preparing to report your supply data” guidance on our guidance page.

-

If the desiccant pack has 2 or more sides that are 2” or less, they should be reported in the small format category of the outer casing’s material (paper, plastic, etc). If the desiccant pack does not qualify as small format, it would be reported as the material category for the outer casing (paper, plastic, etc).

Labels should be reported with the material they are stuck to. For example, if you stick a shipping label to a corrugated shipping box, the label weight should be reported with the cardboard.

-

Report Validation

CAA will perform report validations and may contact producers for clarification or to verify additional data.

This step ensures that all reported information meets the required standards and aligns with program guidelines.

Substantiation Requests

As previously described, when reporting to CAA, producers must submit all methodologies used for data preparation.

Upon request, producers may be asked to provide additional calculations, substantiation for updates, or estimates to confirm the data's reasonability.

This practice promotes fairness and supports accurate fee-setting across all producers.

Producer Compliance & Enforcement

Per ORS 459A.869(8), CAA will establish a searchable registry disclosing all CAA’s compliant members and non-compliant members.

CAA will monitor compliance byconducting periodic audits.

CAA will first notify a non-compliant producer of any deficiency and provide the producer an opportunity to respond and to cure the delinquency.

For any program year that a producer is found to be non-compliant because they are not reporting and paying fees accurately or on-time, the producer will retroactively pay all fees during the period of non-compliance, subject to any interest payments or liquidated damages.

In the event that CAA is unable to adequately resolve a non-compliance:

CAA will send a notification to DEQ after completing its internal compliance processes, and

producers may also be subject to DEQ enforcement fines or penalties.

-

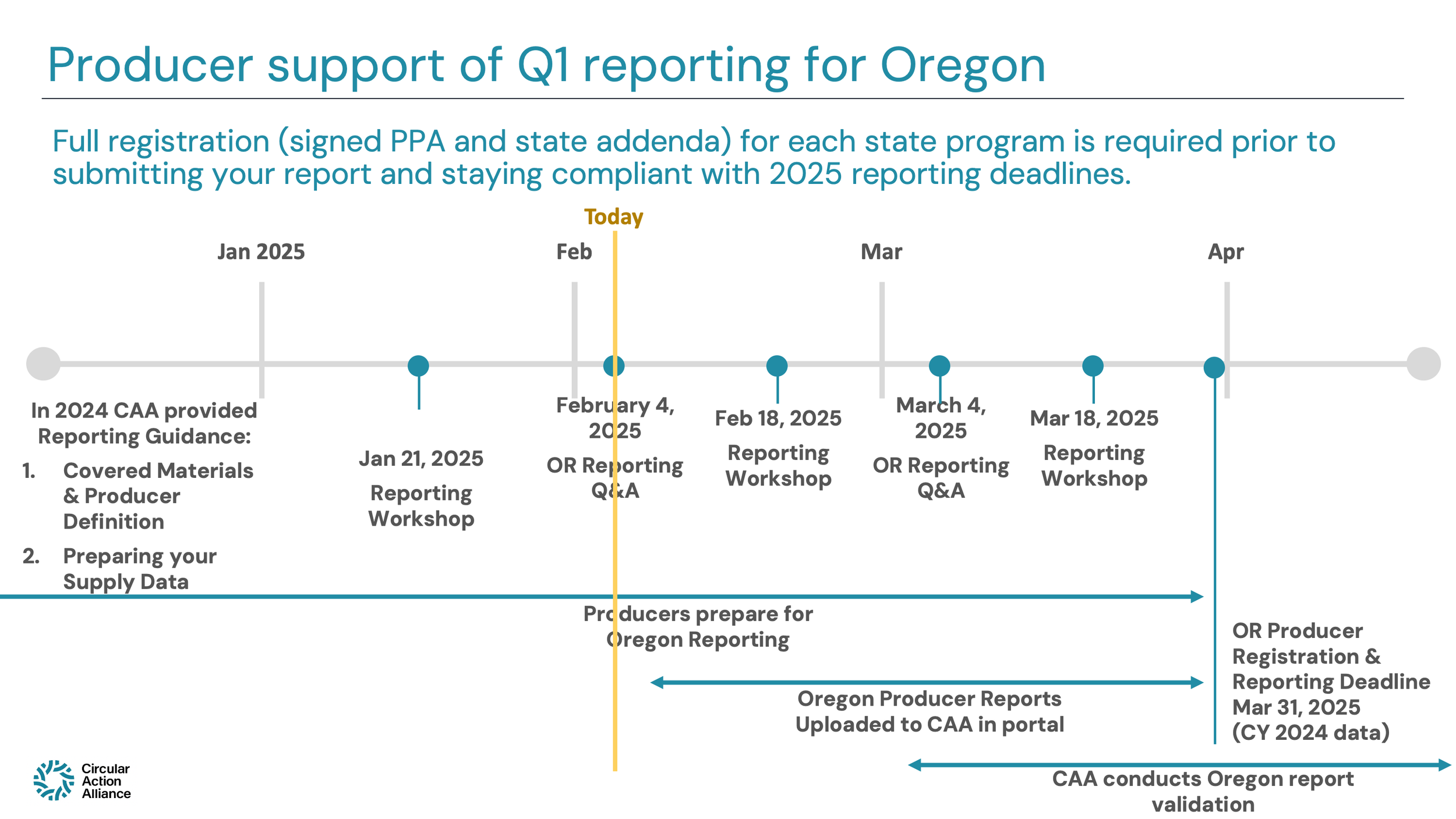

Oregon’s March 31, 2025, reporting deadline and there is no planned extension.

-

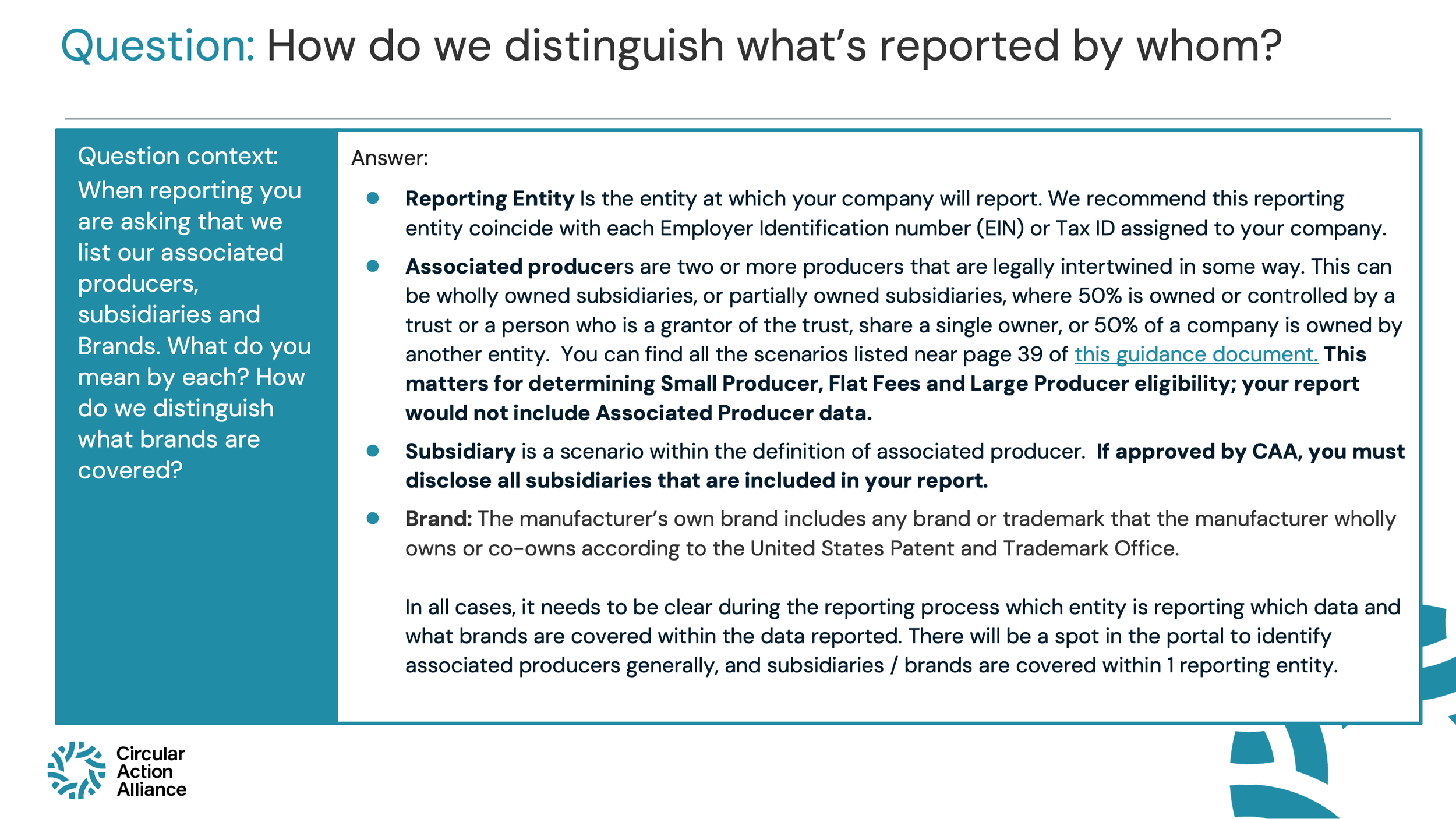

Reporting Entity Is the entity at which your company will report. We recommend this reporting entity coincide with each Employer Identification number (EIN) or Tax ID assigned to your company. If approved by CAA, you must disclose all subsidiaries and brands that are included in your report.

In all cases, it needs to be clear during the reporting process which entity is reporting which data and what brands are covered within the data reported. There will be a spot in the portal to identify associated producers generally, and subsidiaries / brands are covered within the reporting entity.

You can find out more in the “Covered Materials & Producer Definitions: Colorado and Oregon” guidance on our guidance page.

-

For producers that meet one or more of the following criteria in the obligated producer exemptions listed in each state may qualify as exempt based on what’s qualified in the guidance. You can find more information on pages 25-45 in the Covered Materials & Producer Definitions: Colorado and Oregon guidance document on our guidance page.